How A Safety Net Unraveled

Long-term care for the elderly in America faces an affordability crisis. A key component of that crisis is the scarcity of insurance policies covering routine care costs for people as they age. Only about 4% of Americans aged 50+ and 10% aged 65+ have long-term care (LTC) insurance, but an estimated 70% of them will eventually require LTC.

How did the U.S. population end up with ubiquitous (albeit flawed) health insurance coverage, but remarkably little LTC insurance coverage?

In part, the explanation is base rate neglect. People either don’t recognize that most Americans eventually require LTC, or they predict they’ll be in the lucky minority who doesn’t. They don’t buy policies because they don’t anticipate needing them.

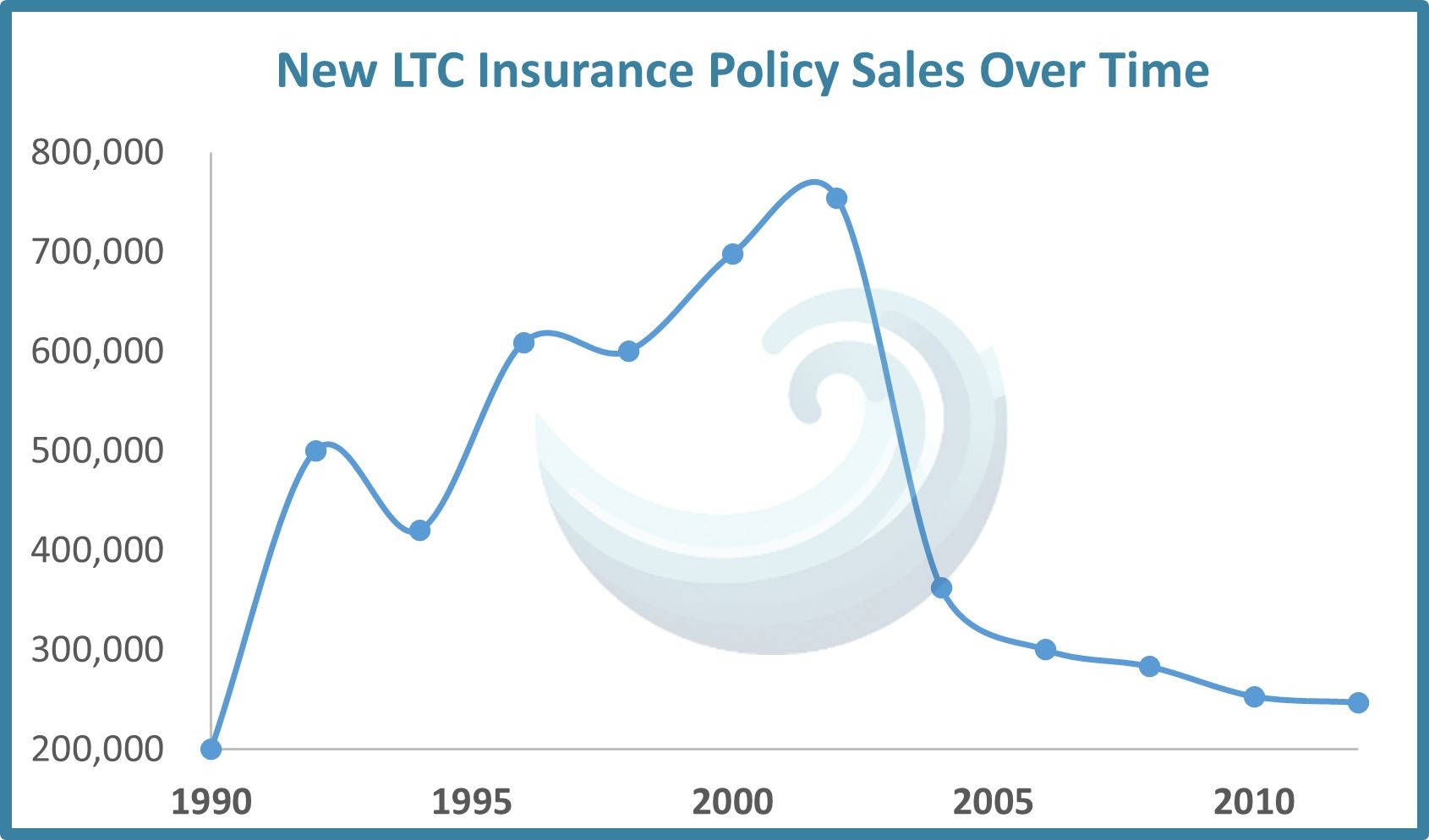

However, there’s an additional, more complex explanation: the LTC insurance market is broken. After a surge in the 1990s, new policy sales plummeted and never recovered. Why?

Understanding Long-Term Care

First, three quick primers:

- The phrase “long-term care” refers to extended use of skilled nursing facilities, assisted living facilities, and home care agencies. LTC is provided over months or years to assist people who need ongoing help to live comfortably.

- Medicare and health insurance don’t cover LTC. They do cover short-term, rehabilitative care with skilled nursing facilities or home health agencies during recovery from surgeries or medical episodes, typically for 30-90 days. Once open-ended care is required, the fuzzy line between “healthcare” and “long-term care” gets crossed, and Medicare and health insurance cease coverage.

- With limited exceptions (e.g., VA benefits), there are only three ways to pay for LTC: cash, Medicaid, or LTC insurance. Seniors only qualify for Medicaid if they have few or no assets. Seniors with assets therefore either (i) have LTC insurance to cover care costs, or (ii) pay cash until they either pass away or deplete their assets and become eligible for Medicaid.

The median annual cost of LTC is about $70k in assisted living facilities, $130k in skilled nursing facilities, and nearly $300k at home. The unfortunate combination of high LTC costs, high LTC utilization, and minimal LTC insurance coverage is partially explained by market failures.

The Catastrophic Mistakes of the 1990s

In the 1990s, LTC insurance carriers made several catastrophic underwriting errors that led to steep losses and caused numerous carriers to exit the market. Now, it’s a concentrated industry with high premiums and slim coverages. Many would-be policy buyers don’t believe the benefits are worth the costs, and new policy sales are a fraction of what they used to be.

Carriers made four key mistakes in the 90s:

1. Underestimated lifespan. Average U.S. life expectancy increased by about five years between 1990 and 2020. This increased the duration of LTC utilization and insurance payouts.

2. Overestimated health-span. Although Americans now live longer, they’re sicker. Increased rates of obesity, metabolic disease, cancer, and other chronic conditions led to higher payouts.

3. Overestimated policy termination rates. Carriers expected more people to cycle off policies before requiring payouts, but most people wound up keeping them for life.

4. Overestimated investment returns. Carriers couldn’t have predicted 15 years of zero interest rate policy. Because these policies are long-duration liabilities, insurers relied heavily on long-duration fixed income instruments that were devalued and/or paid minimal coupons during the ZIRP era. Carriers now suffer from huge asset-liability mismatches.

The Result

This combination of errors led to lower-than-anticipated investment returns and higher-than-expected payouts, resulting in carrier consolidation, increased policy premiums, and reduced coverage.

As the cost to provide – and therefore receive – LTC services continues to rise, LTC insurance has become largely inaccessible. This leaves most Americans responsible for their own care costs.